If you’re behind on your taxes and feeling like there’s no way, you are not alone. Thousands of Americans struggle with tax debt every year. The good news? The IRS offers a program called the Offer in Compromise (OIC), a form of tax debt relief that lets you settle your debt for less than you owe.

Sounds great, right? But before you can apply, the IRS needs to know one thing: how much it can realistically collect from you. That’s where the term Reasonable Collection Potential (RCP) comes in. It’s one of the most important parts of the Offer in Compromise Pre-Qualifier, and understanding how it works could make or break your application.

Let’s break it down step by step.

What Is an Offer in Compromise?

An Offer in Compromise is basically a deal between you and the IRS. It allows you to settle your tax bill for less than the full amount if paying the total would cause financial hardship.

Here’s the key idea:

The IRS doesn’t want to force you into bankruptcy. Instead, it wants to collect what is reasonable based on your current financial situation. If your finances show that you truly can’t afford to pay the full amount, they might agree to accept less.

However, not everyone qualifies. The IRS carefully reviews your financial information, and that’s where the Offer in Compromise Pre-Qualifier tool comes in handy.

How the Offer in Compromise Pre-Qualifier Helps

Before you go through the full application process, the IRS lets you use a free online tool called the Offer in Compromise Pre-Qualifier. It’s designed to give you a quick idea of whether you might qualify for an OIC.

The tool asks about your:

- Monthly income and expenses

- Household size

- Assets like your car, home, or savings

- Debts and living costs

Once you enter this information, the tool estimates something called your Reasonable Collection Potential (RCP). Basically, your RCP is how much the IRS thinks it could collect from you based on your financial situation.

If your RCP is less than your total tax debt, you might be a good candidate for an Offer in Compromise. If it is higher, you may need to explore other tax relief options.

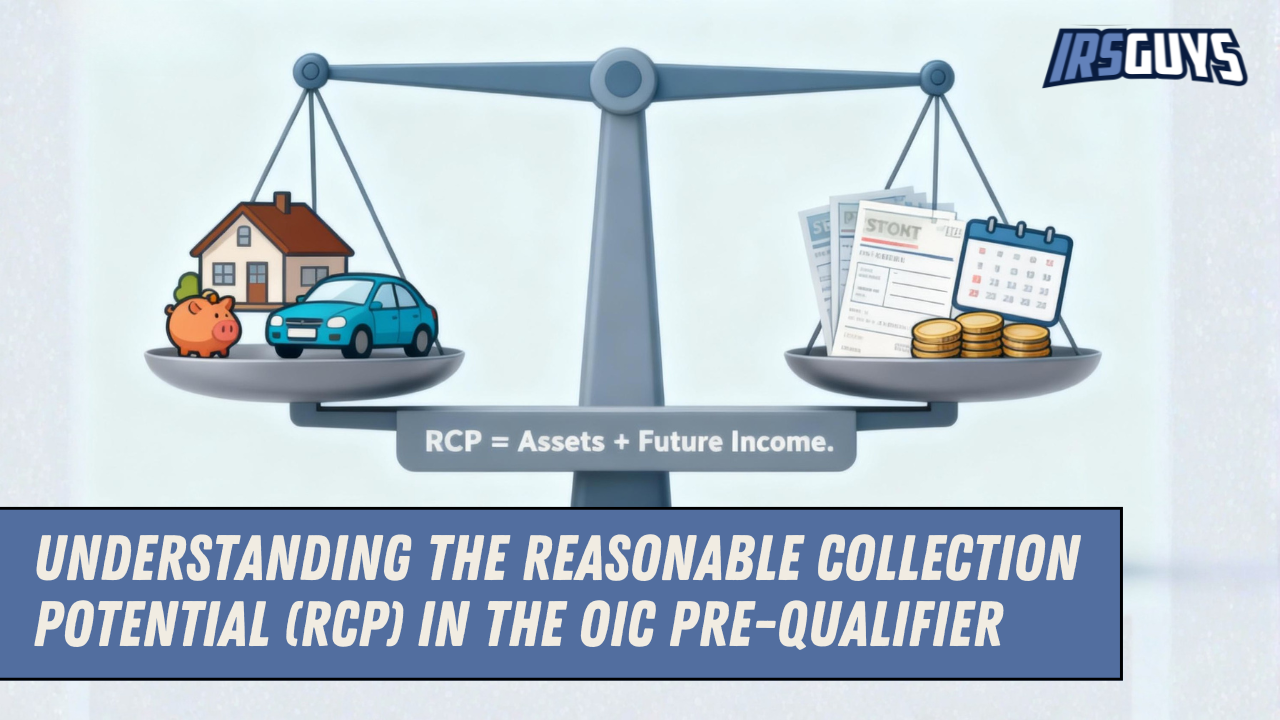

So, What Exactly Is Reasonable Collection Potential (RCP)?

Think of your RCP as your “affordable payment limit.” It’s the total amount the IRS believes they could get from you, either by collecting from your assets or your future income.

Here’s a simple way to think about it:

RCP = Net Equity in Assets + Future Income

Let’s break that down.

Net Equity in Assets

This includes things you own that have value (like your house, car, savings account, or retirement fund).

But don’t worry, the IRS doesn’t count the full market value. They consider what’s called net realizable value, which means what you’d actually get if you sold the item after paying off loans or fees.

Future Income

This is what the IRS expects you to earn going forward, minus reasonable living expenses. They typically multiply your monthly disposable income by 12 (if you plan to pay off your OIC in 5 months or less) or by 24 (if you plan to pay over 6-24 months).

So, if your disposable income is $300 a month and you pick the 24-month plan, your future income portion is $7,200.

And your net equity and future income together — that’s your Reasonable Collection Potential.

Common Mistakes People Make When Estimating RCP

Even though the Pre-Qualifier tool is helpful, many taxpayers make small errors that lead to big problems later. Here are a few common mistakes:

- Listing full asset values instead of net values: For example, if your car is worth $10,000 but you still owe $8,000, your equity is only $2,000 (not $10,000).

- Ignoring IRS expense standards: The IRS uses national and local standards for what they consider “reasonable living expenses.” Even if you spend more in real life, they’ll only allow what fits those standards.

- Forgetting to account for shared household expenses: If someone else in your home helps pay for bills, you’ll need to show that in your calculation.

- Not double-checking before applying: Submitting incorrect numbers can get your Offer in Compromise rejected right away.

Final Thoughts: Don’t Guess Your Way Through RCP

The Reasonable Collection Potential is the IRS’s way of deciding whether you can afford to pay your tax debt in full. Understanding how it works can save you time, frustration, and money.

Before you start your application, use the Offer in Compromise Pre-Qualifier to get a quick idea of where you stand.

Lastly, you don’t have to face the IRS alone. IRS Guys help you turn a confusing process into a clear path toward freedom from tax debt.